.gif)

|

Signature Sponsor

By Michael Crabtree

July 3, 2018 - This article is intended for those of you who are at the beginning of your investing journey and want to better understand how you can grow your money by investing in CONSOL Coal Resources LP (NYSE:CCR).

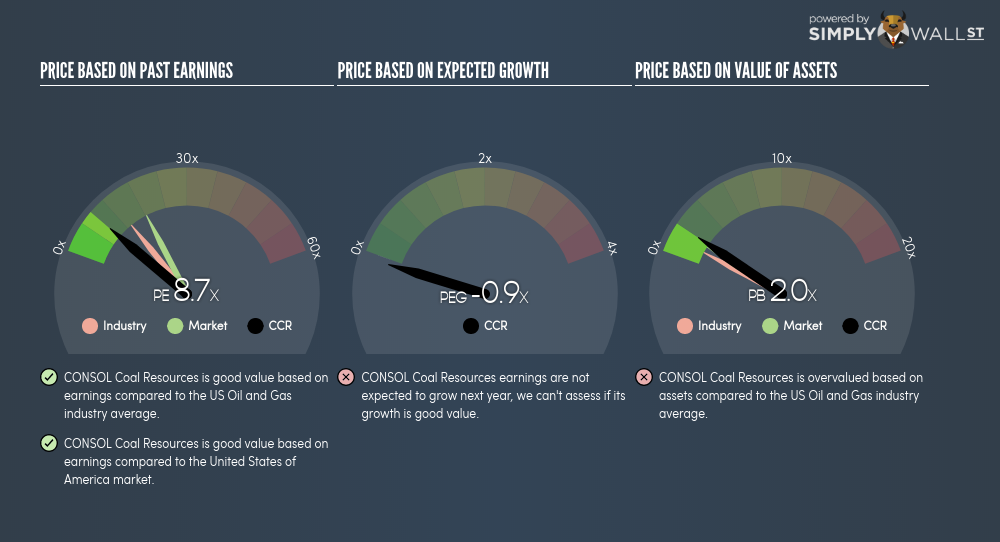

CONSOL Coal Resources LP is currently trading at a trailing P/E of 8.7x, which is lower than the industry average of 13.5x. While CCR might seem like an attractive stock to buy, it is important to understand the assumptions behind the P/E ratio before you make any investment decisions. In this article, I will explain what the P/E ratio is as well as what you should look out for when using it.

Breaking Down the P/E Ratio

A common ratio used for relative valuation is the P/E ratio. It compares a stock’s price per share to the stock’s earnings per share. A more intuitive way of understanding the P/E ratio is to think of it as how much investors are paying for each dollar of the company’s earnings.

Formula Price-Earnings Ratio = Price per share ÷ Earnings per share P/E Calculation for CCR Price per share = $15.1 Earnings per share = $1.727

∴ Price-Earnings Ratio = $15.1 ÷ $1.727 = 8.7x

The P/E ratio isn’t a metric you view in isolation and only becomes useful when you compare it against other similar companies. Ideally, we want to compare the stock’s P/E ratio to the average of companies that have similar characteristics as CCR, such as size and country of operation. A quick method of creating a peer group is to use companies in the same industry, which is what I will do. Since similar companies should technically have similar P/E ratios, we can very quickly come to some conclusions about the stock if the ratios differ.

At 8.7x, CCR’s P/E is lower than its industry peers (13.5x). This implies that investors are undervaluing each dollar of CCR’s earnings. This multiple is a median of profitable companies of 25 Oil and Gas companies in US including Energem Resources, Silver Star Energy and Far Vista Petroleum. Therefore, according to this analysis, CCR is an under-priced stock.

Assumptions To Watch Out For

However, before you rush out to buy CCR, it is important to note that this conclusion is based on two key assumptions. The first is that our “similar companies” are actually similar to CCR. If the companies aren’t similar, the difference in P/E might be a result of other factors. For example, if you inadvertently compared lower risk firms with CCR, then investors would naturally value CCR at a lower price since it is a riskier investment. Similarly, if you accidentally compared higher growth firms with CCR, investors would also value CCR at a lower price since it is a lower growth investment. Both scenarios would explain why CCR has a lower P/E ratio than its peers. The second assumption that must hold true is that the stocks we are comparing CCR to are fairly valued by the market. If this assumption does not hold true, CCR’s lower P/E ratio may be because firms in our peer group are being overvalued by the market.

What This Means For You

You may have already conducted fundamental analysis on the stock as a shareholder, so its current undervaluation could signal a good buying opportunity to increase your exposure to CCR. Now that you understand the ins and outs of the PE metric, you should know to bear in mind its limitations before you make an investment decision. Remember that basing your investment decision off one metric alone is certainly not sufficient. There are many things I have not taken into account in this article and the PE ratio is very one-dimensional.

CoalZoom.com - Your Foremost Source for Coal News |

|