Coking Coal - The Strategic Raw Material

September 4, 2020 - Steel is one of the most widely used materials in the world with an immense variety of applications, including consumer goods, transport, construction, and infrastructure. Steel production has more than doubled this century from 850 Mt in 2000 to 1870 Mt in 2019. Urbanisation and industrialisation create a strong demand for it, particularly in Asia. Coking coal is a vital component of the majority of steel production.

Most steel (71% in 2018) is produced using iron from a blast furnace (BF) which is then treated in a basic oxygen furnace (BOF). The BF-BOF process for iron and steel production starts with the manufacture of high-carbon content coke from coking coal. The coke is then used directly in the BF with iron ore, limestone and oxygen to produce pig iron. Pig iron is mixed with recycled steel, lime and dolomite in the BOF to produce crude steel. The production of 1 t of hot metal in the BF-BOF process requires 1.37 t iron ore, 0.78 t coking coal, 0.1 t thermal coal, 0.16 t PCI coal, 0.27 t limestone and 0.125 t scrap steel. The BF-BOF process accounts for about 9% of total global energy requirements.

The remaining 30% of steel is produced from electricity-based methods, mainly electric arc furnaces (EAF). The furnace is charged with scrap steel and some pig iron from the BF process. The direct reduction iron (DRI) furnace method also relies on scrap steel and pig iron from BFs. Thus, coking coal plays an important role in almost every method of global steel production.

Just over 1000 Mt of coking coal was produced in 2018, accounting for 14% of world coal production. Generally, coking coal costs more than steam coal and its market is limited to the steel industry. In 2018 most coking coal was mined in just five countries: China (523 Mt), Australia (179 Mt), Russia (93 Mt), USA (72 Mt), and India (49 Mt).

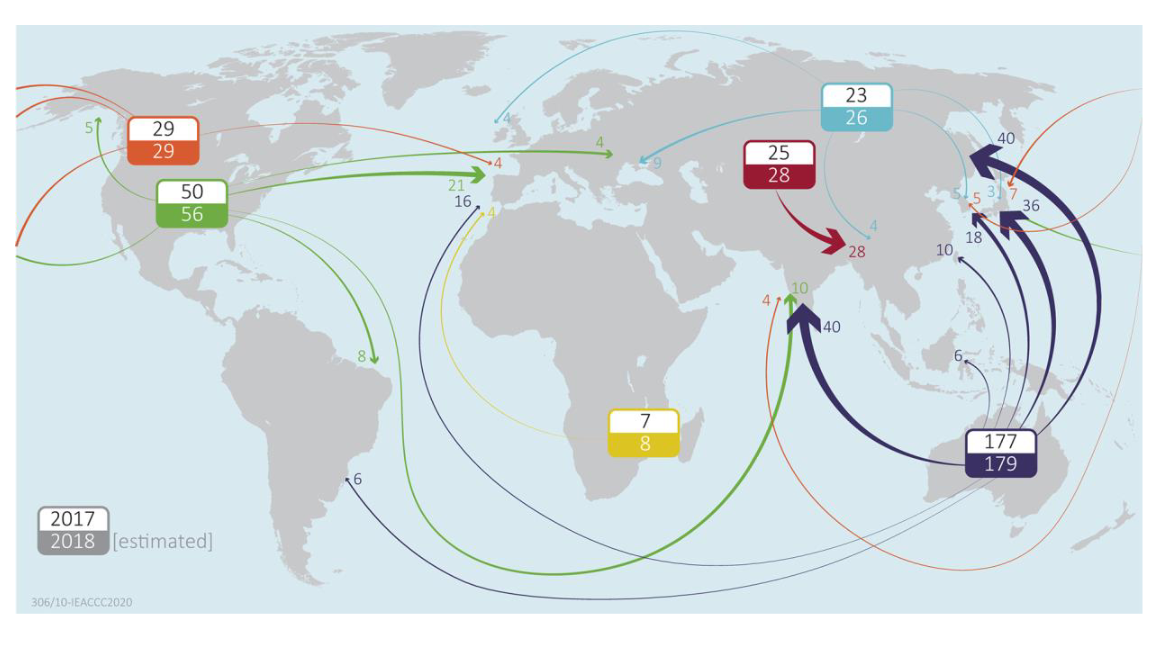

Around 80% of coking coal is used domestically; thus, approximately one-fifth is sourced internationally from the seaborne market. The map shows trade flows of coking coal from the major suppliers to some large users. Australia is the principal exporter of coking coal due to its vast reserves of high-quality coal, modern transport infrastructure, and ease of access to ports. Other suppliers include North America and Russia. Europe still imports coking coal, but it is Asia, which accounts for 70% of world steel production and relies heavily on BF-BOF plants. The pattern of trade over the long term will shift due to the structural decline of coal markets in advanced economies, notably Europe. Major coking coal exporters such as Russia and North America have made preparations to invest in infrastructure that will divert more coal towards Asia.

Map of world coking coal trade in 2017 and 2018 (IEA, 2019b)

Steel is an important part of the fabric of modern life and is also critical to the production of renewable energy. As a general rule, every 1 MW of wind capacity requires roughly 103 t of stainless steel and 20 t of cast iron. This translates to around 78.7 t of coking coal for 1 MW of wind capacity, factoring in the amount of steel produced from EAF and scrap steel used during the BF-BOF process.

Global carbon emissions from iron and steel production were 2.8 Gt in 2017 and are growing. Making greater use of recycled steel and replacing older BF-BOF plants with EAF plants reduces emissions as EAF production produces 400 kgCO2/t of crude steel, BF-BOF emits 1700-1800 kgCO2/t, and DRI emits 2500 kgCO2/t. Emissions from BF-BOF plants themselves can be reduced by the greater use of scrap metal, further energy efficiency measures, and productivity improvements throughout the plant. Innovations such as incorporating carbon capture and storage (CCS), or replacing coke with hydrogen, syngas, or biomass in the form of charcoal, are all being developed and could play a role in reducing CO2 emissions from the integrated steel plant. Even as alternatives are deployed, the role of coking coal will remain significant in the medium to long term.

The IEA Clean Coal Centre is organised under the auspices of the International Energy Agency (IEA) but is functionally and legally autonomous. Views, findings and publications of the IEA Clean Coal Centre do not necessarily represent the views or policies of the IEA Secretariat or its individual member countries.

Each executive summary is based on a detailed study which is available separately from www.iea-coal.org. This is a summary of the report: Coking coal – the strategic raw material by Paul Baruya, CCC/306, ISBN 978-92-9029-629-4, 106 pp, August 2020.