|

Signature Sponsor

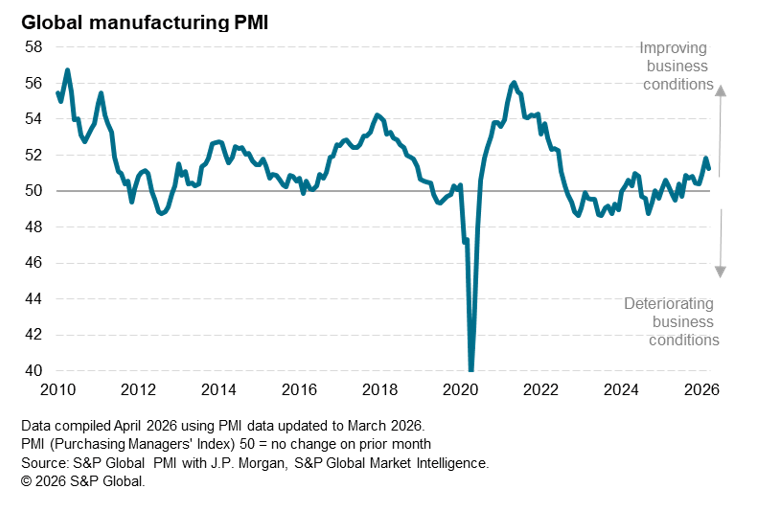

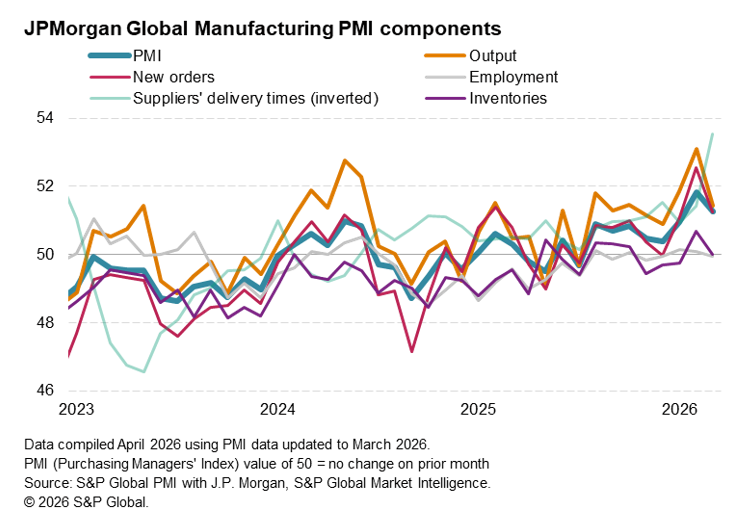

April 1, 2026 - Global manufacturing continued to grow in March, according to PMI survey data, the rate of expansion slowing but displaying encouraging resilience in the face of surging energy prices and supply delays. However, the forward-looking indicators hint at these pressures playing a greater role in dampening growth in the months ahead. Manufacturing PMI dips on war impact The global manufacturing recovery has been knocked off course by the outbreak of war in the Middle East. Having risen to a 44-month high of 51.8 in February, the headline manufacturing Purchasing Managers’ Index (PMI), sponsored by J.P. Morgan and compiled by S&P Global Market Intelligence, fell to 51.3 in March.

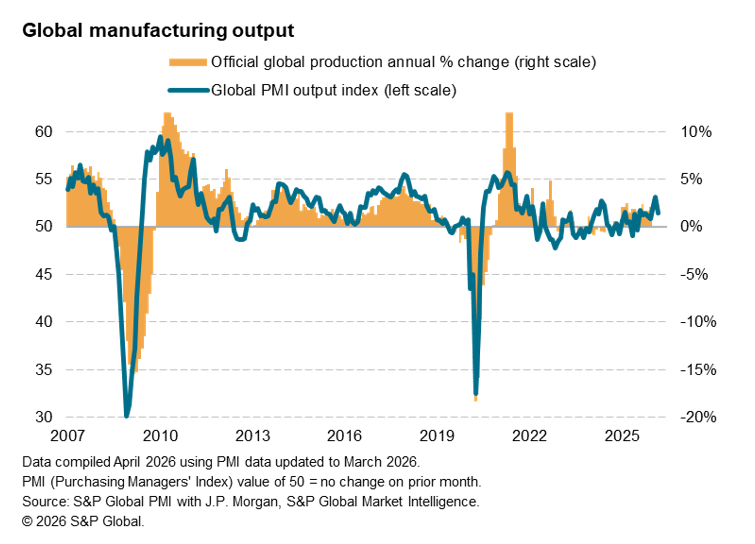

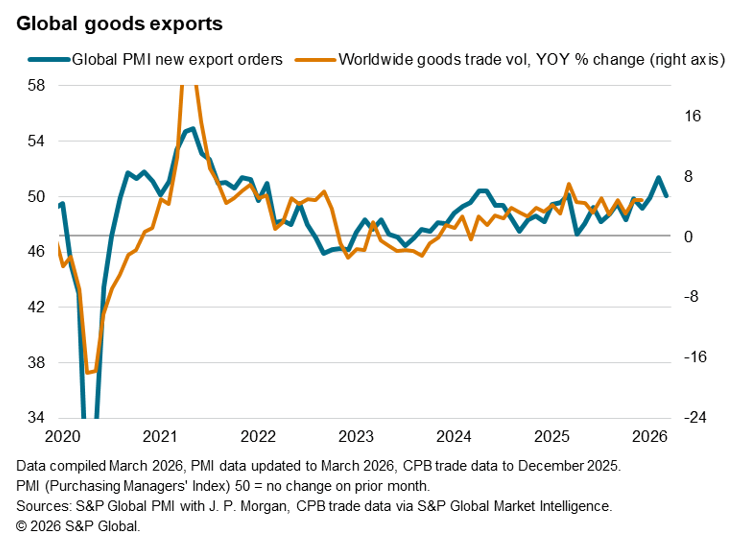

While still above 50, the PMI remains in growth territory for an eighth successive month, and March’s reading was in fact the second-highest seen over the past 45 months. But the relative resilience of this headline indicator masks a more worrying picture of deteriorating demand growth, surging prices and supply chain delays, all of which threaten to push growth lower in the coming months. In the first instance, it should be borne in mind that the headline PMI is a composite of five survey variables. Of these five PMI components, the output index fell in March to signal a slowing of production growth to a three-month low, driven by a cooling of new orders growth globally. Order book growth in turn weakened due to a near-stalling of global trade flows, which represents a disappointing pull-back in global goods export flows after February had seen the strongest rise for over four years.

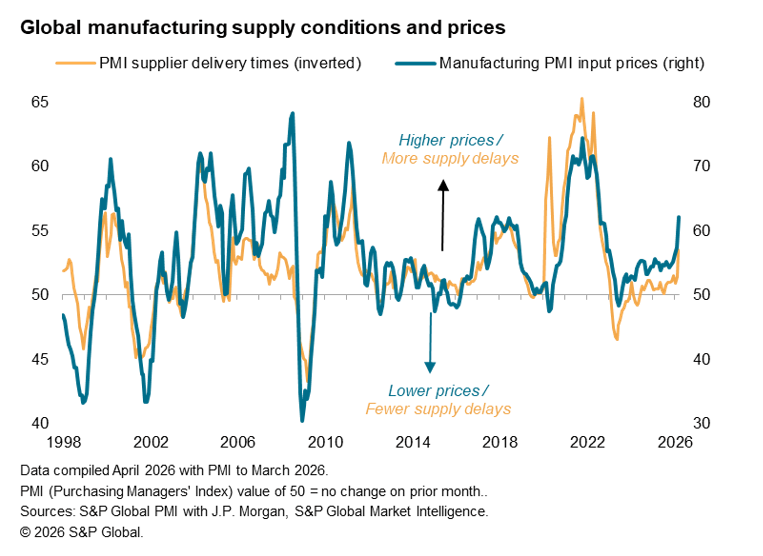

This change in the demand environment contributed to an ongoing reluctance to add to headcounts, with employment unchanged after two months of marginal gains as firms on sought to reduce staffing overheads. Stocks of purchased inputs were also unchanged after having risen in February, likewise reflecting cost-cutting. However, the biggest change in the five variables which comprise the PMI was seen in the suppliers’ delivery times index, which signalled the greatest degree of global supply chain delays since October 2022. Worsening delivery delays were generally associated with the impact of the war in the Middle East, and notably the knock-on effects of the halting of shipping through the Strait of Hormuz.

Watching the sub-indices The added complication is that the suppliers’ delivery times index is inverted in the calculation of the PMI, such that worsening supply conditions act to buoy the PMI. This is because, in normal trading conditions, longer delivery times are typically a symptom of strong sales causing demand to outstrip supply. However, in the current situation, as had also been seen during the pandemic, the lengthening of supply times is instead being caused by a supply shock. Hence the PMI is being boosted by what is in reality a negative factor, albeit one that should in theory spur greater investment in boosting supply in the coming months. However, for now, it means the strength of the headline PMI should be treated with caution, and instead we urge users to focus on the sub-indices behind the PMI. Confidence slides as prices jump Two other key indices, which are not components of the PMI, sent particularly important signals in March. First, business expectations fell globally among the PMI survey panels to the lowest since last October. This deterioration is a disappointment after business confidence had shown promising signs of recovering in the opening months of 2026. Optimism had climbed to a 21-month high in February amid moderating concerns over US tariff policy. Not surprisingly, the outbreak of war at the end of February has been the principal factor behind this relapse, taking the forward-looking indicator of the survey to a level back below the long-run average.  A key element of the pull-back in confidence was the war-related surge in energy prices recorded in March. Average input prices rose globally at the fastest rate since July 2022, the rate of inflation accelerating to a degree not seen since December 2009. Higher energy prices were widely reported, though prices of other inputs also rose as high oil and gas prices fed through to other commodities, including food and chemicals, and shortages further flamed price pressures.

Average selling prices also rose at a sharply increased rate, the rate of inflation hitting highest since November 2022, as producers sought to pass the cost increase on to customers to protect margins. The key concern among manufacturers is that higher prices alongside the uncertainty caused by the geopolitical environment will dampen demand in the months ahead, especially if the price spike becomes persistent and if central banks turn more hawkish in this inflationary environment. |

|