|

Signature Sponsor

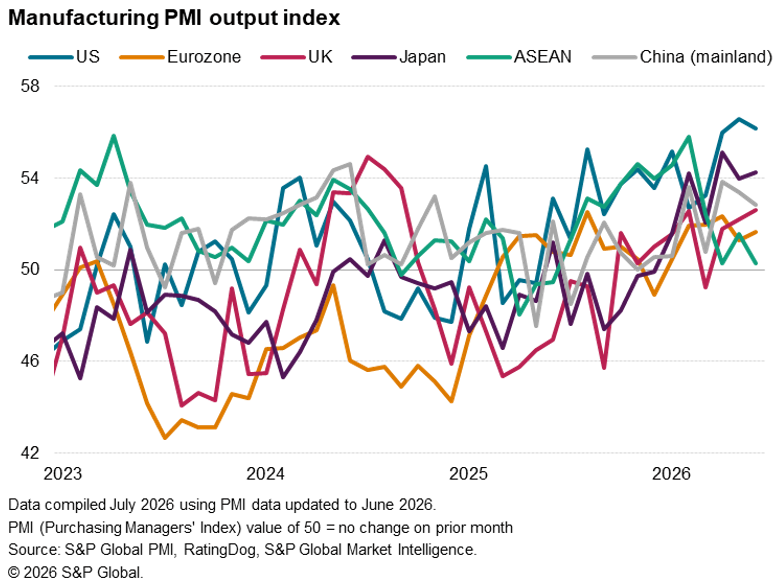

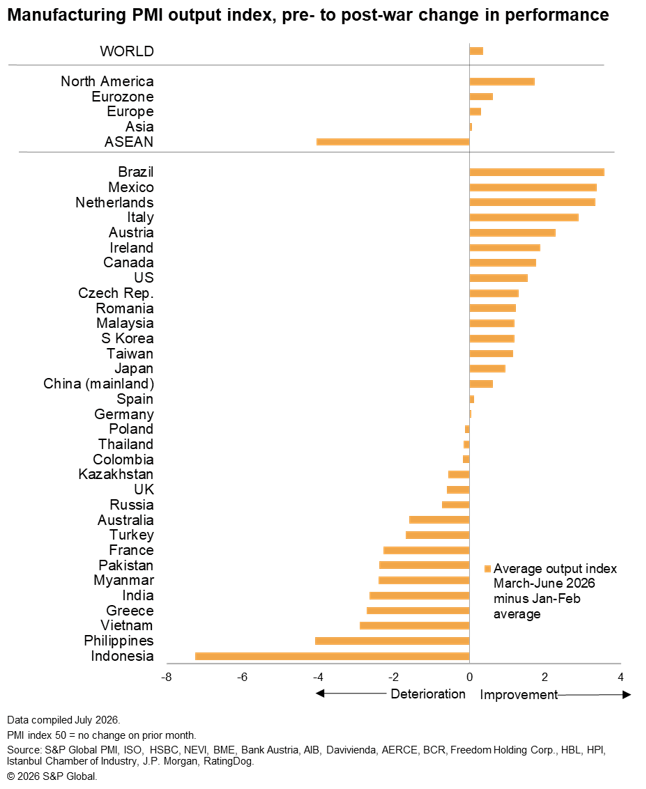

July 3, 2026 - PMI® survey data highlight a widening growth differential between major regions and economies around the world since the outbreak of the war in the Middle East. Notably stronger performances in North America, led by the US, alongside growth spurts in recent months in Japan, Taiwan, South Korea and – to a lesser degree – mainland China, contrast with a near-stalling of growth in the ASEAN region, the latter indicating a sharp reversal of fortunes after an especially strong start to the year. North American growth spurt contrasts with ASEAN slowdown The worldwide Manufacturing Purchasing Managers’ Index™ (PMI) surveys compiled by S&P Global Market Intelligence have recorded strongly divergent production trends around the world since the outbreak of the war in the Middle East on 28 February. Regionally, the biggest improvement has been evident in North America, according to comparisons of the PMI Output Index averaged in the four months since the outbreak of war (encompassing the March to June period) against the first two months of the year. By far the sharpest deterioration in performance has meanwhile been reported in the ASEAN region, where growth in the second quarter has come close to stalling. Performance across the broader Asian manufacturing economy as a whole has meanwhile been largely unchanged, though with a pocket of strong growth seen in East Asia. Elsewhere, the Eurozone, and to a lesser extent the wider European economy, has seen a modest improvement.

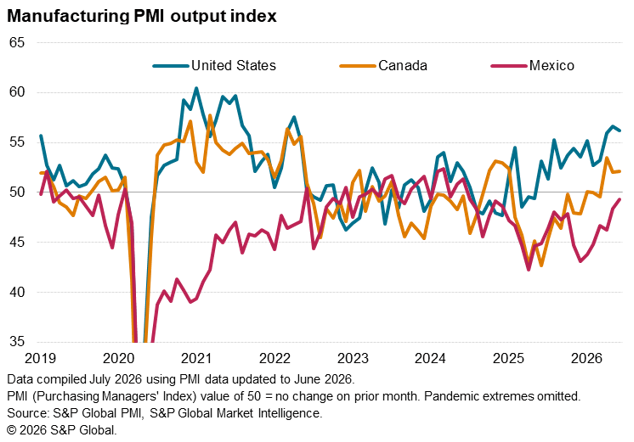

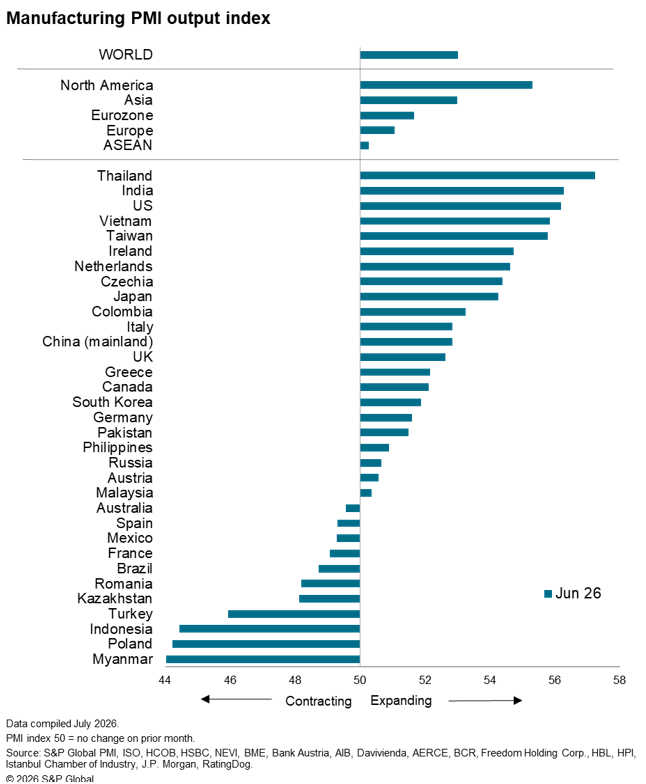

North American growth spurt After Thailand and India, the US reported the fastest manufacturing output growth in June, rounding off its strongest quarterly expansion since the third quarter of 2021 to provide a key impetus behind the improved performance in North America. Growth in Canada during June meanwhile completed its best quarter since the end of 2024, and Mexico’s long-running tariff-related downturn came close to stabilising after its decline moderated in June to the slowest for just under two years.

Japan ends best quarter for over a decade as East Asia booms Strong performances were by no means limited to North America, with notably robust gains evident in East Asia. Aided by an historically weak exchange rate, Japan’s factories reported the largest expansion of output since the first quarter of 2014 during the three months to June, while both South Korea and Taiwan notched up their best quarters for five years. Mainland China meanwhile enjoyed its best quarter of growth for two years. Outside of Asia, the UK rounded off its strongest quarter of growth for nearly two years and the eurozone closed off its best quarter since the start of 2022. Although mixed performances were seen within the single currency area: strong expansions in the Ireland and Netherlands contrasted with weakness in France and Spain, while Germany continued to report modest growth. ASEAN slowdown In the ASEAN region, performance varied in June from the top-ranking growth in Thailand to a further downturn in politically disrupted Myanmar, which sat at the foot of the growth rankings. However, the biggest deteriorations in performance in the post war period compared to the opening two months of the year worldwide were seen in Indonesia, the Philippines and Vietnam, dragging overall growth in the region close to a standstill. Outside of ASEAN, weaker performances were also seen in Australia and Brazil, with output falling in June, as well as in many central and eastern European economies. Strong-performer Czechia notably bucked the regional trend here.

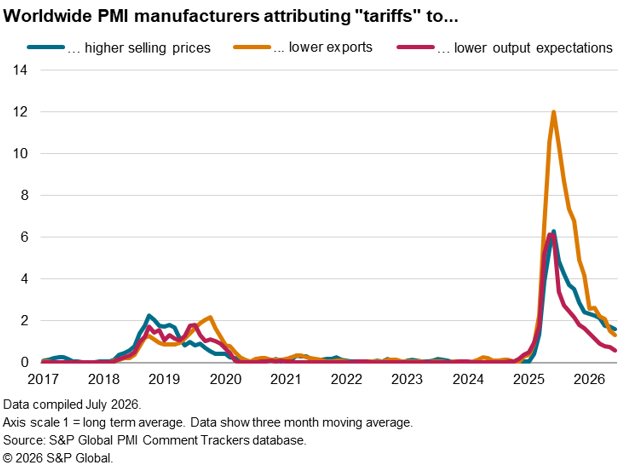

Assessing growth drivers and demand dampeners Some caution is needed in assessing underlying growth rates for some of the better-performing economies, as demand has been buoyed in many instances since the outbreak of war in the Middle East by precautionary stock building. This inventory building has boosted both output and order books, though with some of the beneficial impact waning in June. However, there are other factors driving growth, notably including the AI build-out and a reduced detrimental impact from tariffs. Reports of tariffs having caused higher prices, lower exports and reduced growth expectations have fallen sharply since peaking in the second quarter of last year.

Where growth has weakened, companies often attributed declining output growth to reduced input availability due to the shipping disruptions from the closure of the Strait of Hormuz, as well as broader supply constraints, which are running at one of their highest since 2022. But dampened customer demand due to resistant to higher prices, in turn linked to higher energy prices and supply scarcities, has been a further major factor denting sales and production growth. See “Global PMI shows sustained manufacturing growth surge, but future optimism fades” for more details on the drivers and dampeners of growth in June. |

|